Asheville Short-Term Rental Regulations: Permits, Zoning, and the 2026 Rules Hosts Must Follow

Asheville bans whole-home STRs in most zones. Here is what the homestay permit actually requires, how taxes stack to 16.75%,…

Asheville bans whole-home STRs in most zones. Here is what the homestay permit actually requires, how taxes stack to 16.75%,…

Savannah's STVR rules are among the most detailed in Georgia. Learn the permit types, cap system, tax obligations, and enforcement…

Miami and Miami Beach operate under entirely different short-term rental rules. Miami Beach's $20,000 starting fine is not a typo.…

Arizona's short-term rental regulatory landscape has changed dramatically since the 2016 preemption law. Here is what Scottsdale Airbnb and VRBO…

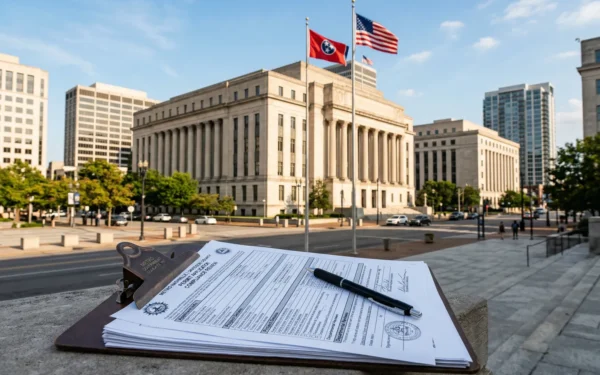

Nashville's STR rules are detailed, strictly enforced, and full of zoning distinctions that can catch investors off guard. Here is…

Houston's first comprehensive STR ordinance took effect January 1, 2026. Registration, $1M liability insurance, human trafficking training, and fines up…

Austin's updated STR ordinance hits platforms on July 1, 2026. License display requirements, delist enforcement, and occupancy limits mean hosts…

The One Big Beautiful Bill Act permanently restored 100% bonus depreciation for STR property acquired after January 19, 2025. Here…

California SB 346 brings platform accountability. Rhode Island doubled STR taxes. Austin requires license numbers by July 1. The EU…

The FIFA World Cup 2026 kicks off in four months. Here's a city-by-city breakdown of STR permits, tax obligations, and…